Can You Use Apple Pay with Crypto in 2026?

Yes, but not the way most people expect. Apple Pay doesn't hold crypto. It doesn't settle payments on a blockchain. In crypto buying flows, Apple Pay works as a fiat payment method rather than as a blockchain payment rail.

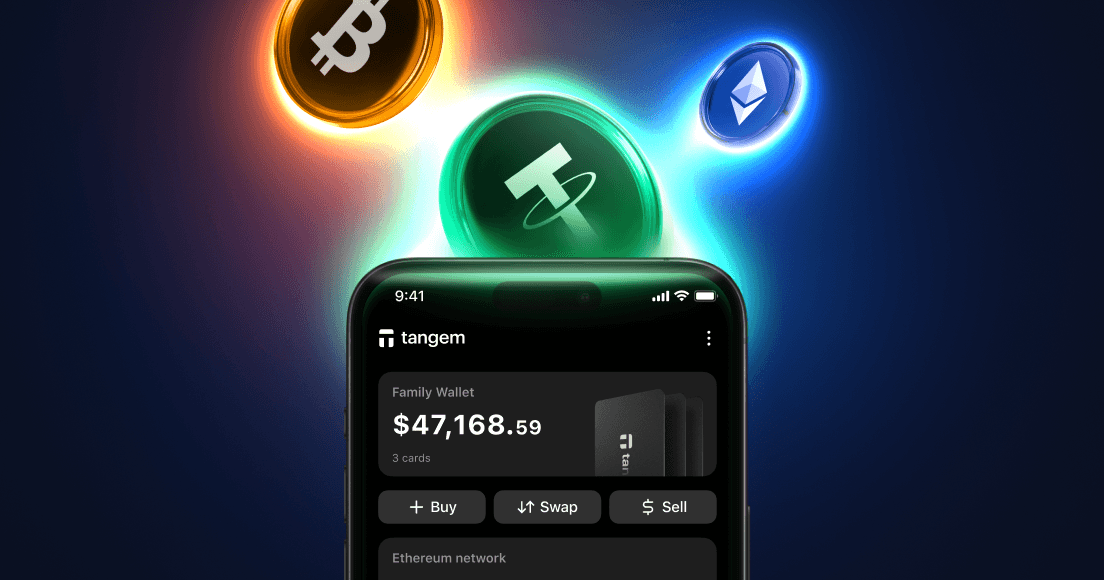

What has changed is the card setup around it. Tangem Pay is a virtual Visa card built into the Tangem Wallet app. You load it with USDC on the Polygon network, add the card to Apple Wallet, and from that point, you tap to pay exactly like you would with any other card in Apple Pay. Your USDC funds the card balance. The Visa network handles the transaction. The merchant receives USD. That's the short answer. Here's how it actually works.

Why Apple Pay Doesn't Support Crypto Natively

Apple Pay is a fiat card payment method, not a crypto wallet or a blockchain payment rail. When it appears in crypto apps, it is typically used to authorize a card-funded purchase rather than to send assets on-chain. There's no crypto anywhere in that chain. Under the hood, Apple Pay uses tokenized card credentials. When you add a card, the payment network or issuer creates a device-specific account number for that phone. At checkout, your iPhone presents that token and a transaction-specific security code. The terminal still routes a normal card payment through normal card networks.

When people talk about "buying crypto with Apple Pay," they mean something different: they're using Apple Pay as a payment method inside a crypto exchange app to fund a purchase. Apple Pay authorizes a card payment to the exchange, which then buys crypto on its own rails. No, blockchain transfers happen inside Apple Pay. This is why using crypto with Apple Pay requires a translation layer. You need something that holds USDC on-chain, converts it to a spendable Visa balance, and presents that balance to Apple Pay as a card. Tangem Pay does that job. Your USDC funds the card balance. The Visa network handles the payment. Apple Pay is the delivery mechanism.

You're not spending crypto at the terminal. The spend comes from a virtual Visa card that you loaded with USDC. The distinction matters, because it's exactly why this setup works.

How to Add Tangem Pay to Apple Pay: Step-by-Step

Step 1: Download the Tangem app (iOS). The app is free and available on the App Store. Your iPhone needs to be running iOS 16.0 or higher on an iPhone 8 or newer.

Step 2: Complete onboarding. Open the app and set up your Tangem Wallet. If you already have a Tangem hardware wallet card, tap it to the back of your phone to pair it.

Step 3: Activate Tangem Pay. Navigate to the Tangem Pay section in the app and tap "Get Started." You'll be prompted to complete identity verification (KYC) through Sumsub, which requires a valid government ID and a selfie. KYC is mandatory. It's a regulatory requirement for the Visa card layer, and it's handled by regulated partners in compliance with applicable laws. Tangem itself does not see or store your identity data.

Step 4: Load USDC to your Tangem Pay card. Once approved, you need USDC on the Polygon network in your Tangem Wallet. Send the amount you want available for spending to your Tangem Pay account. A small Polygon gas fee applies. This is a network fee paid to validators, not to Tangem. Your top-up becomes spendable after blockchain confirmation. That matters for beginners because the card balance is not the same thing as the wallet balance shown elsewhere in the app. Move only the amount you want available for everyday payments. Keep the rest in your main Tangem Wallet.

Step 5: Add to Apple Wallet. In the Tangem app, find your Tangem Pay card and follow the prompts to add it to Apple Wallet. Apple Wallet will ask you to verify the card. Complete that verification as prompted.

Step 6: Pay. Use Apple Pay contactless at supported in-store terminals. Your Tangem Pay card appears in Apple Wallet as a virtual Visa card. Set it as your default card to trigger it automatically at checkout.

What Happens When You Tap to Pay

Here's the sequence behind a single Tangem Pay purchase through Apple Pay:

- You double-click and authenticate with Face ID or Touch ID.

- Apple Pay presents your Tangem Pay virtual Visa card for contactless payment.

- The merchant's terminal processes a standard Visa card transaction.

- The Visa network settles the transaction in USD. The merchant receives USD.

- Your Tangem Pay card balance is reduced by the purchase amount in USD. USDC from your card balance funded the transaction at a 1:1 rate (1 USDC = 1 USD).

The merchant sees a normal Visa transaction. Nothing about the payment signals that crypto was involved. Say you load 40 USDC to Tangem Pay and use Apple Pay for a 25 USD purchase at a Visa contactless terminal. Apple Pay presents the card credential, the Visa network processes the payment, and your Tangem Pay balance drops by the equivalent amount. Your remaining USDC stays in the card account.

For purchases in non-USD currencies, standard Visa FX rates apply to convert the purchase amount to USD before it is deducted from your balance.

Tangem Pay Works for Contactless and Online Payments

Once the card is in Apple Wallet, Tangem Pay supports the payment surfaces confirmed in the dossier.

iPhone: tap to pay at Visa contactless terminals in stores.

Online: for websites that don't support Apple Pay at checkout, you can enter the virtual card details directly: card number, expiry, and CVV, at any Visa-accepting online checkout.

This gives Tangem Pay two practical roles. On the phone, it behaves like a contactless card inside Apple Wallet. Online, it behaves like a standard virtual Visa card. The same funded card balance supports both use cases, so you do not need a separate spending balance for web checkout. Tangem Pay also supports Google Pay on Android. The setup process is the same: add the virtual Visa card to Google Pay from within the Tangem app.

One clarification worth making: current Tangem Pay support includes iPhone-based Apple Pay and online card entry. The Tangem app requires iOS 16.0 or later on iPhone 8 or later, and it has no desktop or web interface.

What You Need to Know Before You Start

A few things are worth understanding before you load your first USDC.

KYC is required. Identity verification through Sumsub is mandatory to activate Tangem Pay. There's no anonymous card issuance. This is a regulatory requirement for the Visa card layer, not a Tangem policy choice. Your main Tangem Wallet, by contrast, requires no KYC and collects no personal data. Only Tangem Pay activity is visible to compliance partners.

USDC on Polygon specifically. Your USDC must be on the Polygon network. A USDC balance on Ethereum mainnet or another chain won't directly fund your Tangem Pay card. If it sits on a different network, you'll need to bridge it to Polygon first. The Tangem app supports cross-chain swaps via multiple providers, so this is manageable, but it's worth noting.

No monthly fee. No transaction fee. Tangem Pay has no monthly account fee, transaction fee, or virtual card issuance fee. The costs you'll encounter are Polygon gas when topping up your card (paid to network validators, not Tangem) and standard Visa FX rates for non-USD purchases. Subject to applicable limits and merchant restrictions.

Your card balance is separate from your wallet. Only the USDC you explicitly transfer to Tangem Pay is available for spending. Your main Tangem Wallet holdings, whatever else you hold across 100+ supported networks, are not connected to the card balance and are not at risk if your card is compromised. Freezing a Tangem Pay card disconnects it from the Visa network, but the on-chain USDC balance is unaffected.

That separation is the core safety model for daily spending. You can keep long-term holdings in Tangem Wallet and move a smaller amount into Tangem Pay when you want card access. Freezing the card stops Visa network purchases. You do not freeze the rest of your wallet.

Availability. Tangem Pay launched in the USA, Latin America, and Asia-Pacific (across 42 countries). UK and EU availability was planned for 2026. Check current availability for your region before starting setup. Regional rollout matters because Tangem Pay is tied to a regulated card account. Apple Pay support on your phone is not enough by itself. You also need Tangem Pay to be available where you live, and your card use remains subject to applicable limits, eligibility checks, and merchant restrictions.

Here's the honest limitation worth naming: Tangem Pay is a virtual card only. Physical cards are planned for future release, but if you need one in hand today, that option isn't available yet.

Conclusion

Apple Pay doesn't support crypto natively, and that's not changing. But the translation layer now exists. Tangem Pay lets you load USDC on Polygon to a virtual Visa card, add that card to Apple Wallet, and tap to pay at Visa-accepting merchants, with no monthly or purchase fees and no bank account required. Your crypto stays in self-custody until you choose to move it to your card balance. The Visa network handles the rest. Ready to set it up? Visit tangem.com/en/tangem-pay/.

FAQ

-

No. Apple Pay transmits tokenized Visa or Mastercard credentials to merchant terminals via NFC. The transaction settles in fiat through traditional card networks. Tangem Pay bridges crypto and Apple Pay by acting as a virtual Visa card funded with USDC. Your USDC funds the card balance, and the Visa network handles the payment.

-

Via Tangem Pay, the supported funding token is USDC on the Polygon network. Other cryptocurrencies are not currently supported as card funding. If you hold a different token, you'd need to swap it to USDC on Polygon before topping up your Tangem Pay card.

-

Tangem Pay has no monthly, transaction, or virtual card issuance fees. A small Polygon gas fee applies when you load USDC to your card balance. That fee goes to network validators, not to Tangem. Standard Visa FX rates apply for purchases made in non-USD currencies. Subject to applicable fees and limits.

-

Apple Pay uses tokenization. Your actual card number is never transmitted to the merchant. KYC identity verification via Sumsub is required to activate Tangem Pay, adding a layer of regulatory compliance to the card. Your main Tangem Wallet remains fully private: no KYC, no collection of personal data, and your transaction history and holdings are not visible to Tangem Pay compliance partners. Security also depends on keeping the two balances separate in your head. Tangem Pay is the spending account. Tangem Wallet is where your main holdings live. A card freeze affects the Visa connection for Tangem Pay purchases, not your hardware-wallet keys or your broader wallet balance.

-

Freezing your Tangem Pay card disconnects it from the Visa network, so it can't be used for purchases. Your on-chain USDC balance is not affected by a freeze. The funds remain in the smart contract you control. You can unfreeze the card and resume spending when you choose.

-

No. Tangem Pay and Tangem Wallet are separate. Your main wallet holdings are not connected to the card balance. Only the USDC you explicitly transfer to Tangem Pay is available for card spending. A compromised or frozen Tangem Pay card has no effect on your Tangem Wallet private keys or holdings.