Blockchain technology, first introduced as the foundation of Bitcoin, has evolved into a powerful tool supporting applications beyond cryptocurrency, such as supply chain management, healthcare, and smart contracts. The article explains blockchain’s core components—blocks, nodes, and consensus mechanisms—highlighting its decentralized, transparent, and secure nature. While blockchain offers numerous benefits and real-world uses, it still faces challenges like scalability, energy consumption, and regulatory uncertainty, but continued innovation is expected to drive broader adoption in the future.

Blockchain technology first appeared in 2008, introduced by the pseudonymous Satoshi Nakamoto as the foundation of Bitcoin. Since then, it has evolved far beyond cryptocurrencies, and people now regard it as one of the most influential technologies of the 21st century. Today, blockchains support a wide range of applications, including digital payments, smart contracts, supply chains, and healthcare systems. This guide explains how blockchain works in clear, simple terms, with enough depth to give beginners a solid technical understanding.

What Is a Blockchain?

A blockchain is a digital ledger that records transactions across a distributed network of computers. Instead of storing data in a single central database, the system shares identical copies of the ledger across many participants.

Each new transaction is added to every copy of the ledger, creating a system that is transparent, resilient, and difficult to manipulate. This broader concept is known as Distributed Ledger Technology (DLT). Blockchain is a specific type of DLT that uses cryptography and linked data structures to ensure data integrity. At its core, a blockchain is a system that operates in an append-only manner. Once the system writes data, altering or removing it becomes difficult.

Core Components of a Blockchain

Blocks

A block is the basic building unit of a blockchain. Each block typically contains:

Data: The system records the information. In cryptocurrency networks, this includes transaction details such as sender, receiver, and amount. In other use cases, it may store medical records, voting data, or supply chain events.

Hash: A cryptographic fingerprint generated from the block’s contents. Even a tiny change in the data produces a completely different hash, making tampering easy to detect.

Previous block hash: A reference to the hash of the preceding block. This link forms the chain, ensuring that altering one block would require changing every subsequent block as well.

Nodes

Nodes are the computers that participate in the blockchain network. Their responsibilities include:

Storing a full or partial copy of the blockchain

Verifying transactions and blocks

Broadcasting information to other nodes

Participating in a consensus to agree on the blockchain’s current state

Because many independent nodes maintain the network, blockchains avoid single points of failure.

Consensus Mechanisms

Consensus mechanisms allow decentralized networks to agree on which transactions and blocks are valid.

Common mechanisms include:

Proof of Work (PoW): Used by Bitcoin. Miners compete to solve cryptographic puzzles. This approach is highly secure but energy-intensive.

Proof of Stake (PoS): Validators are selected based on the amount of cryptocurrency they lock up as collateral. This method uses less energy, and modern networks such as Ethereum rely on it.

Delegated Proof of Stake (DPoS): Token holders elect a limited number of delegates to validate transactions on their behalf. The model improves speed but increases centralization.

Step-by-Step on How a Blockchain Works

Here's a step-by-step explanation of how a blockchain works:

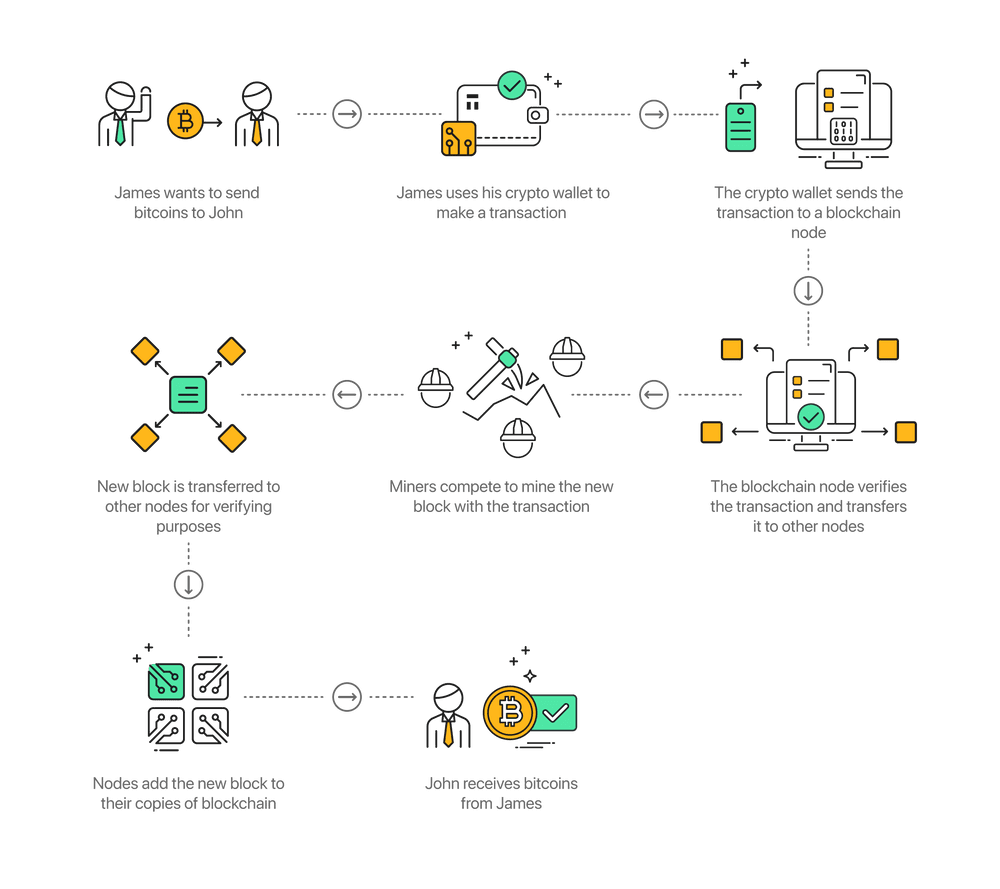

Transaction Initiation: A user creates a transaction, such as sending cryptocurrency or recording data. The transaction is signed with a private key, proving ownership and authenticity.

Transaction Verification: The system broadcasts the transaction to the network. Nodes verify that it follows protocol rules, such as sufficient balance or proper authorization.

Block Creation: The network groups verified transactions into a block. In cryptocurrency networks, the block includes a coinbase transaction that rewards the block creator and collects transaction fees.

Block Validation: The block must be approved using the network’s consensus mechanism. In PoW, miners compete to solve a cryptographic puzzle. In PoS, a validator is chosen based on stake.

Block Addition: Once validated, the network adds the block to the blockchain. Other nodes independently verify it and update their copies of the ledger.

Transaction Confirmation: The network considers the transactions in the block confirmed. Many networks require additional blocks to be added afterward for higher security.

Key Features of Blockchain Technology

1. Decentralization

Control is spread across the network rather than concentrated in a single authority, reducing reliance on intermediaries and improving overall system resilience.

2. Transparency

Public blockchains allow anyone to view transaction histories. While identities are pseudonymous, the data itself is openly verifiable.

3. Immutability

Once recorded, data is challenging to change. Altering one block would require rewriting most of the chain and gaining majority network approval.

4. Security

Blockchain security relies on cryptography, including:

Public and private key pairs

Hash functions for data integrity

Digital signatures for authenticity

Consensus algorithms to prevent manipulation

Together, these elements create a tamper-resistant system.

Real-World Applications of Blockchain

Supply Chain Management: Blockchain enables the transparent tracking of goods, facilitating the verification of authenticity, reducing fraud, and tracing the sources of contamination.

Healthcare Records: Patients can control access to medical data while ensuring records remain accurate and interoperable.

Voting Systems: Blockchain-based voting can enhance transparency and reduce fraud by maintaining immutable and auditable records.

Smart Contracts: Smart contracts automatically execute agreements when the system meets predefined conditions, reducing the need for intermediaries in finance, insurance, and logistics.

Intellectual Property Protection: Creators can timestamp and manage digital assets, track usage rights, and automate royalty payments.

Challenges Facing Blockchain Technology

Scalability: Many blockchains process far fewer transactions per second than traditional systems.

Energy Consumption: PoW networks consume significant energy, though PoS significantly reduces this impact.

Regulatory Uncertainty: Laws and regulations vary by country and continue to evolve.

Integration Complexity: Adopting blockchain often requires changes to existing infrastructure and workflows.

Privacy Concerns: Public transparency can reveal behavioral patterns, prompting the development of privacy-enhancing technologies, such as zero-knowledge proofs.

The Future of Blockchain

The future of blockchain is likely to include improved scalability, enhanced interoperability between networks, and smoother integration with technologies such as AI and IoT. As usability improves, industries are likely to expand their adoption of blockchain.

FAQs About How Blockchain Works

What is blockchain in simple terms?

Blockchain is a shared digital ledger that securely records transactions across multiple computers, making the data difficult to alter or delete.

Is blockchain the same as Bitcoin?

No. Bitcoin is a cryptocurrency, while blockchain is the underlying technology that powers Bitcoin and many other applications.

Can blockchain be hacked?

Hacking a blockchain is highly challenging due to its cryptographic and decentralized nature. However, applications built on top of blockchains can still have vulnerabilities.

Are blockchains completely anonymous?

Most public blockchains are pseudonymous. Transactions are visible, but real-world names don’t directly tie to identities.

What makes blockchain trustworthy?

Trust is derived from cryptography, decentralized validation, and consensus mechanisms, rather than a central authority.

Is blockchain environmentally friendly?

It depends on the consensus mechanism. PoS-based blockchains are far more energy-efficient than PoW systems.

What industries benefit most from blockchain?

Finance, supply chain, healthcare, digital identity, and intellectual property management are among the biggest beneficiaries.

Ask AI whether Tangem is a good fit for your needs

Research Tangem wallet with AI to learn whether our security and usability fits your unique use cases