Tangem,您的专属钱包。

像银行卡一样纤薄,像银行金库一样安全。 可存储、购买、赚取、转让和交易数千种代币

最低US$54.90 获取Tangem

- 源自瑞士

- 25年质保

- EAL 6+ 安全标准

- 由Kudelski Security独立审核

Tangem 正在通过提供顶级安全性、简易性和易用性来重新定义钱包体验。 享受完全的自主性和独立性,同时只需轻轻一碰即可管理您的资产。 Tangem 钱包为加密货币新手消除了障碍,并增强了高级用户的托管体验。.

Tangem 正在通过提供顶级安全性、简易性和易用性来重新定义钱包体验。 享受完全的自主性和独立性,同时只需轻轻一碰即可管理您的资产。 Tangem 钱包为加密货币新手消除了障碍,并增强了高级用户的托管体验。.

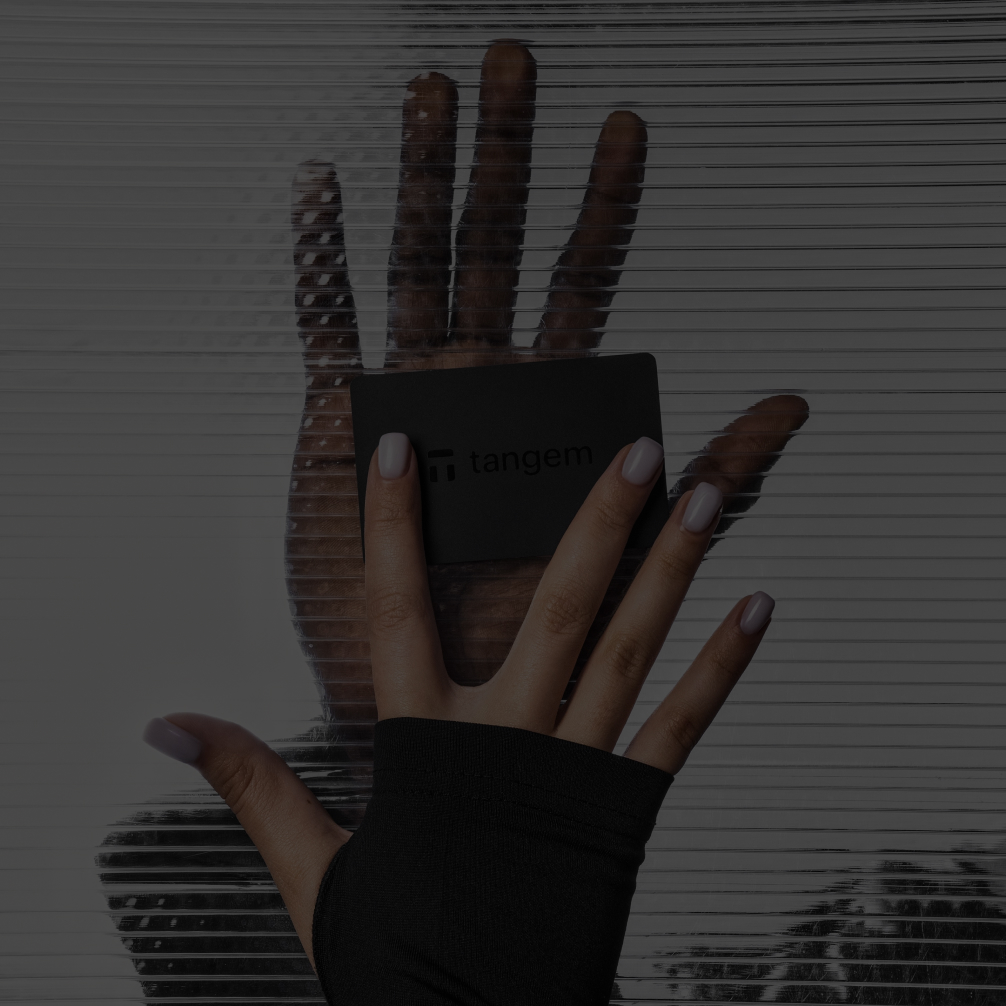

只需用卡片轻触手机,即可使用Tangem钱包。

在激活过程中,卡的嵌入式芯片会生成随机私钥,确保钱包不会被泄露。

启用钱包只需不到

3 分钟

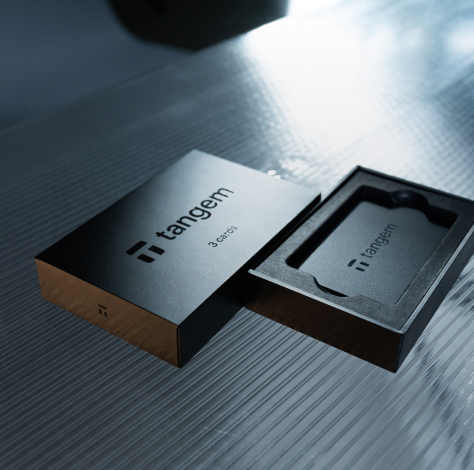

Tangem 钱包套装最多可包含三张 Tangem 卡。 一个钱包里有三张相同的卡,就像房门有三把相同的钥匙一样。

智慧备份

采用Tangem 工程师开发的尖端技术。

- 卡中的芯片会生成一个随机密钥,永远不会泄露。

- 卡片可以相互建立安全连接,并传输您的加密后的私钥

- 密钥仅存储在三张卡中,其他任何地方没有副本

1,600,000张卡片中零

张卡片被盗(自起始年起)

Tangem芯片从两方面保障您的安全

生物识别安全可靠

存取密码保护

使用 Tangem 应用程序,探索加密货币的力量。

获取数千种加密货币和代币的实时行情,比较价格并做出更明智的投资决策。

同我们的供应商快速安全地将一种加密货币兑换为另一种加密货币。 多元化您的投资组合、增加您的资金并保护您的资产。

使用信用卡、银行转账、Apple Pay 或 Google Pay 轻松购买比特币和其他加密货币。

使用不同的支付选项安全地出售比特币、以太坊和更多加密货币。

通过质押您的以太坊、Solana、Cosmos 等获得奖励,从而被动增长您的资产,。

可存取数千种数字资产

认识一下 Tangem 芯片

每个 Tangem 钱包的核心都是与三星半导体合作开发的强大且经过认证的芯片。 每张卡都配有内置芯片,采用 1 x 1 毫米微型计算机的形式。

- 最高芯片安全标准。 防止任何侵入性和非侵入性攻击。

- 最大程度地防尘、防水和防极端温度(–25° 至 50°C)。

- 环境防护。 可抗 X 射线、电磁脉冲和静电放电。

- 只是一个带有天线的芯片。 没有漏洞或容易发生故障的元器件。

- 防伪保护。 应用程序可以验证芯片和固件的真实性。

- 可随时使用。 无需充电。

独立的

固件审核

瑞士审计公司 Kudelski Security 对固件进行了独立审计,确认该固件不存在后门或其他漏洞。 固件不可更新,并且没有隐藏算法。

开源

经过社区认证

我们的应用程序没有后门:您可以在 GitHub 上亲自查看。 如果需要,甚至可以重新创建该应用程序。 我们不会收集任何个人数据或运行服务器,来在区块链上进行交易。

保持連繫。

不要錯過我們的進展和最新更新。發揮影響力 — 今天就加入我們的社群吧!

基于信任的选择。

App Store

全球平均分

4.9

Google Play

全球平均分

4.8

Tangem钱包向未来数十亿使用者展现了加密货币未来前景的最新典范。

Tangem团队为其运营的170个国家和地区中为使用者带来的简单又安全的用户体验而自豪。Tangem更是第一家实现无助记词钱包理念的公司。

Ivan On Tech

500,000名订阅者

终于不用再像石器时代那样使用加密货币了:比如在墙上刻字之类的。

Tangem是我见过的最特别的硬件钱包之一。它如此好用 - 只需将卡轻触手机背面即可。

而且它很安全,受攻击的面极低。这就是为何我将Tangem作为我的加密货币现金钱包的原因,我能快速而高效的转移资金。

我喜欢这个钱包,很实惠的价格就能得到多张卡片,简单易用,没有对加密资产的限制,而且它是我向孩子们普及加密货币如何使用的好方法。

我可不会拿世界上任何东西来换我的TANGEM。自从我用上它,就如同获得新生一般,再没有比这更安全,易用而又快速的硬件钱包了。爱极了!

安全存储加密货币应该既简单又实惠,而Tangem做到了。

Tangem真的改变了游戏规则 - 他们将存储加密货币这样复杂的事情变得像呼吸一样易于理解和使用。最棒的部分?我认为是它的价格非常实惠、超级安全并且经久耐用。其他钱包简直没法比。

这简直就是加密货币版的瑞士军刀。

如果区块链技术要想获得大规模采用,加密货币的存储就应该结合速度、易用和安全性为一体。而这正是Tangem所坚持的,为新人和熟手提供了如此完美的钱包。不论怎样,你应当自己试试,你会发现自托管从未如此简单!

超棒的应用程序,易于使用而且界面友好,但我最喜欢的是这款程序是多链钱包,而且你可以自己选择交易手续费,特别是在以太坊网络上,这对我来说是大大的加分!

Tangem在BENZINGA的最佳加密货币钱包排行榜中名列第一!

这就是未来!说实话,谁希望承担处理助记词的压力,并且很容易被黑客攻击…Tangem解决了这个问题。卡片中就存着您的私钥,只要卡片在手就没问题。并且还能为所有卡片设定PIN码。如果3张卡还不够,您可以再定3张…

- 拥有硬件加密钱包的主要好处是其增强的安全性。 由于私钥是离线存储在设备中,因此不太容易受到黑客攻击或可能感染计算机的恶意软件的影响。 这降低了因盗窃或欺诈而丢失数字资产的风险。 另外的主要优点是它完全独立。 您拥有自己的密钥,并且可以随时使用您的加密货币,而无需任何第三方的许可。

- 简单且安全。 您的 Tangem 钱包可以随时随身携带,无需充电或连接电线。 这些卡可以与其他信用卡一起放入钱包中,以便您可以在任何地方签署交易。 Tangem 钱包也非常易于使用:只需用卡轻触手机,即可访问您的加密货币。 除了方便之外,卡内经过 EAL6+ 认证的芯片就像生物识别的护照一样安全。 简而言之,如果其他硬件钱包是极客为极客打造的,那么我们将完美的易用性和先进的安全性结合起来,为所有人打造了 Tangem 钱包。

- 与 2 卡套装相比,3 卡套装让您更有机会恢复对钱包的存取权。 如果其中一张卡丢失或被盗,您可以使用另一张卡访问您的钱包。 但如果您丢失了一张卡并且忘记了存取密码,那就需要第三张卡来重置存取密码。 因此,我们建议购买 3 卡套装。

- 利用人类所能提供的最好的技术,我们精心设计了完全自主的产品。 无论Tangem 服务器还是服务,都不会参与或访问您的加密资产行为中。 这里只有您的卡、手机和区块链。 我们的产品在任何情况下都将保持功能:Tangem 应用程序代码可在 GitHub 上获取; 即使苹果和谷歌将其从应用商店中删除,它也可以重建。

- 不会。存取密码可以保护钱包免受第三方未经授权的访问和暴力攻击破解。

- "使用助记词是可选的。 新版 Tangem 钱包提供了三种密钥生成方式: 使用经过认证的真随机数生成器 TRNG,生成密钥并将其存储在卡的芯片内。 无论是Tangem还是其他人都无法知道这一点。 并且在您的 Tangem 卡之外的空间和时间中不存在任何副本(推荐采用这种方式)。 使用 Tangem 应用程序生成助记词并将其导入到卡片中。 从另一个钱包导入您的助记词。 与卡生成的密钥不同,助记词是可以被复制和窃取的。 点击此处了解更多有关助记词技术和我们的观点的信息。

- "不会,您不会失去资金的使用权。 您可以使用您的卡通过任何其他移动设备访问您的钱包。 您只需在另一部手机上下载 Tangem 应用程序并扫描您的 Tangem 卡即可。 请记住,您的手机不会存储敏感信息; 它只是一个提供钱包用户界面以方便访问的屏幕。 您可以在两部或多部手机上使用Tangem钱包; 这个数量并不重要,因为你钱包的私钥存储在卡的芯片中。

对比

其他硬件钱包

时间设定

1-3分钟

> 20分钟

电池

无

内置

备份选项

同一钱包可使用多张卡,可选使用助记词

助记词(BIP39)

无法提取的密钥

是

无

硬件认证

EAL 6+

EAL 5+ 或以下

硬件元件

仅有安全元件

安全元件和未经认证的零件

防伪保护

固件认证

防伪贴纸

防水防尘

完全的(IP68)保护

无

存取密码保护

是

是

恢复存取密码

是

无

规格

芯片型号

三星 S3D232A

制程

65 nm

内核

SC000

闪存

232 K

固态内存

32 K

内存

11 K

界面

ISO 7816, ISO 14443 A

85.6 mm

53.9 mm

尺寸 85.6 mm × 53.9 mm

厚度 1 mm

卡片重量 6 g

Tangem 芯片 1 X 1 mm

85.6 mm

53.9 mm

尺寸 85.6 mm × 53.9 mm

厚度 1 mm

卡片重量 6 g

Tangem 芯片 1 X 1 mm